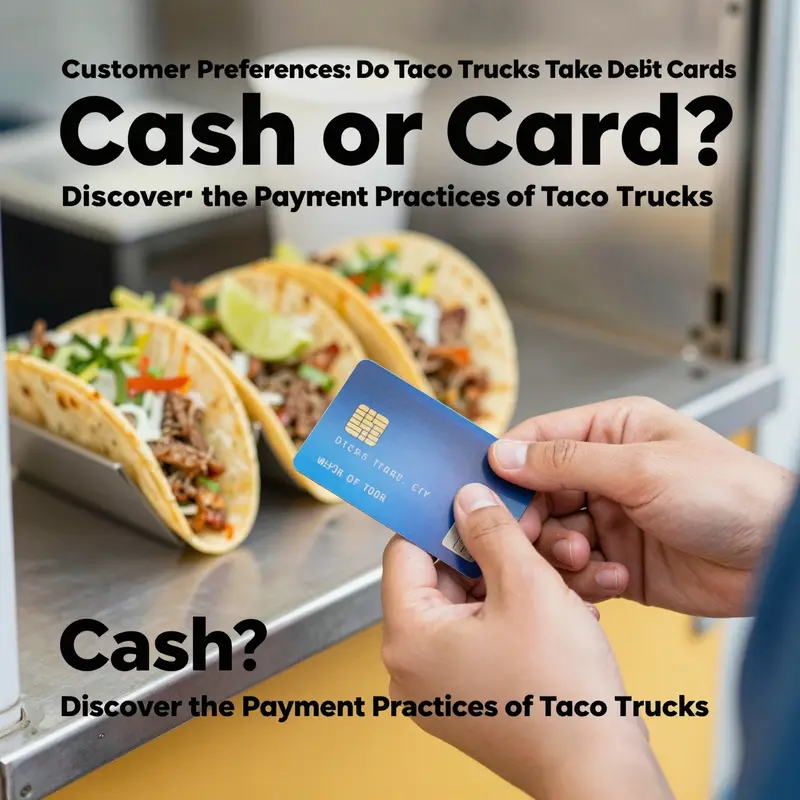

Taco trucks have become an essential part of urban dining, offering delicious, quick bites in a vibrant atmosphere. However, as a savvy urban commuter or city dweller, knowing how to pay can greatly enhance your taco truck experience. Do taco trucks accept debit cards? The answer can vary widely depending on location and the vendor’s preferences. In this article, we’ll explore how payment methods differ across regions, delve into customer convenience preferences, and examine how taco trucks are evolving to meet modern payment demands. Get ready to savor your favorite tacos without the stress of fumbling for cash!

Swipe or Crunch: The Card-Handoff at Taco Trucks

Payments at taco trucks reveal how urban diners expect flexibility. Debit cards are common in many trucks, but cash-only remains in a surprising number of places. The reasons are practical: equipment costs, connectivity, and vendor comfort with technology. For customers, card acceptance can speed lines, provide receipts, and reduce the need to search for cash. Vendors with card readers can reach a broader audience and lower cash-handling risk.

The logistics of a mobile POS matter: it must work outdoors, tolerate weather, and safeguard customer data. Clear signage and online updates indicating accepted methods reduce friction. When a truck advertises card acceptance and tap-to-pay, customers feel reassured that their purchase will go smoothly. The payoff is a quicker checkout, cleaner records, and stronger revenue tracking for the business.

Across cities and neighborhoods, the landscape is a spectrum rather than a single rule. In bustling hubs, card readers are near-ubiquitous; in more remote or cash-preference communities, cash still dominates. Observing this pattern helps readers understand micro-business economics and how small operators balance costs, reliability, and customer expectations. For researchers and enthusiasts, noting whether a truck accepts debit cards is a useful data point about digital adoption, throughput, and inclusivity.

To help shoppers, look for signage at the window, check vendor profiles, or scan reviews for payment details before arriving. For vendors, weighing card acceptance against fees and connectivity can guide decisions that improve service speed and growth while maintaining trust with customers.

Card in the Concrete Jungle: The Evolving Reality of Debit Card Acceptance at Major-City Taco Trucks

In the bustling street-food ecosystems of America’s largest cities, taco trucks have evolved from humble, cash-only fixtures into agile micro-venues that mirror the broader shift toward digital commerce. The question of whether taco trucks take debit cards is no longer a simple yes-or-no trap; it’s a nuanced snapshot of location, vendor philosophy, and the day’s pace. Across urban cores—from sunlit corners of west-coast neighborhoods to the late-night sprawl of eastern urban grids—card payments have become commonplace, yet the landscape remains far from uniform. The result is a city-by-city mosaic where a diner’s card can glide through a reader at one stop and, just blocks away, a truck might still rely on cash, chalking up another reminder that the world of mobile street dining is as diverse as the cities that host it.

The broader trend toward card acceptance is visible in the way operators configure their business models. Larger, established food-truck operations typically run on point-of-sale systems that integrate debit and credit card readers, often coupled with contactless payment capabilities and mobile wallets. In major urban markets, these tech-enabled setups are less a novelty and more an expectation. They streamline the transaction, reduce cash-handling risk, and simplify end-of-day reconciliation. For customers, the experience is frictionless: a quick tap or a wave of the phone, a receipt emailed or texted, and the line moves a little faster. For vendors, the advantages extend beyond speed. Card payments bring digital records, easier inventory control, and the potential for loyalty or promotion programs that can be deployed without the logistical overhead of physical punch-stamps or cash drops. The shift aligns with how payment environments are converging across the restaurant sector, driven by both consumer demand and the practicalities of modern point-of-sale hardware.

Yet the journey from cash to card is not uniform. In many neighborhoods, smaller, independent taco trucks—often family-operated and proudly agile—still operate on a cash-first basis. There are concrete reasons for this conservatism. Transaction fees can be daunting for low-volume vendors who move slowly from street corner to street corner and must cover every cost threshold with thin margins. Some operators voice concerns about the reliability of card readers in high-traffic, outdoor environments where connectivity can be intermittent or where the cost of maintaining off-grid solutions would cut into scarce profits. For another subset, the simplicity of cash matches a lower-tech operational footprint: a portable card reader, a small secure cash box, and a system that rewards speed and minimal setup during peak hours. In those cases, the cash-on-hand approach isn’t stubborn nostalgia; it’s a calculated balance between risk, cost, and the precise rhythms of daily street commerce.

Historical snapshots offer context for today’s reality. A well-known Yelp entry from several years back highlighted a cash-only stance at a California truck, serving as a reminder that the cash-first model wasn’t merely a relic of the past. Those anecdotes matter less as stand-alone proof and more as qualitative markers in a broader dataset. Today, studies and industry reports paint a different picture: card acceptance is increasingly embedded in the street-food fabric of major metros. The National Restaurant Association’s mobile-food trends reports, within the 2025 snapshot, point to a notable shift—well over two-thirds of mobile vendors in major metropolitan areas now accept card payments. The momentum reflects a market that recognizes customer expectations for speed, convenience, and contactless transactions, and it’s reinforced by the deployment of vendor-facing technology that makes card processing straightforward and reliable, even in mobile environments.

A practical way to understand this evolution is to consider how large urban markets differ from smaller neighborhoods. In metropolitan hubs, the density of trucks, the concentration of footfall, and the strategic competition for consumer attention create an incentive to offer multiple payment options. These operators often set up near office districts, college campuses, or transit hubs, where the speed and efficiency of card transactions can reduce wait times and increase throughput during lunch rushes or festival weekends. The choice to adopt debit and credit payment methods aligns with a broader business goal: capture more spend by removing a payment barrier. When a customer reaches the front of the line with a card in hand, there’s no need to turn away while searching for cash or calculating change. In many cases, vendors discover that card readers also simplify tipping, especially in social dining settings where the experience is as much about ambiance and shareable meals as it is about the food.

Smaller operators aren’t immune to this pressure, but they face different pressures. A family-run truck that moves between a handful of fixed patrol points today and a handful more tomorrow might embrace a modest, portable payment setup. These devices can operate offline for periods when connectivity dips, syncing later when a signal returns. The aim is to minimize missed sales due to payment friction. Even with offline resilience, the trend toward card processing remains evident. It’s a question of balancing the cost of card-processing agreements—per-transaction fees, monthly charges, and potential hardware depreciation—against the revenue lift that card acceptance can deliver. For some vendors, the break-even point occurs at higher volumes, where the incremental revenue from card transactions outweighs the consistent, predictable costs of processing.

From a consumer’s perspective, the experience varies with geography and the specific truck’s business model. In the few pockets of the city where cash remains the widely preferred method, it’s usually because the truck operates in a cash-heavy corridor, or it serves a demographic that prioritizes immediate, tangible transactions. In other zones, customers arrive to find a sign or a posted sticker indicating that debit and credit cards are accepted, sometimes accompanied by the option for contactless and, less commonly, digital wallets. The presence of clear payment information matters as much as the payment method itself; it reduces uncertainty and avoids the awkward moment when a line forms and the customer has to ask, “Do you take cards?” The clarity also signals to potential customers that the truck is professional, adheres to basic security and compliance standards, and has integrated a system that can handle receipts and records—an attribute increasingly valued by urban diners who like to track expenses or claim rewards.

For readers who want to connect the dots between infrastructure and payment practices, the logistics of where trucks park and how they access customers is not incidental. The operational backbone—parking networks, street permissions, and event partnerships—often shapes whether a given truck can sustain a card-based operation. A truck anchored near a dense transit corridor might leverage a fixed POS setup, supported by a reliable network and curated event calendars, while another truck that roams night markets, fairs, or pop-up street events may rely on flexible, battery-powered readers and a cash-back-up plan. In practice, a vendor’s decision to accept debit cards frequently hinges on a combination of proximity to high-traffic areas, the reliability of a local payment processor, and the vendor’s appetite for the ongoing costs of card processing. The aim, across scenarios, remains the same: to reduce friction so customers can enjoy the meal without debating payment method mid-line.

Customers navigating this landscape can do a few practical things to prepare. Before setting out, check the truck’s latest social media announcements or listings, as many operators post updated payment policies and accepted methods. For newer or lesser-known trucks, a quick look at review sites can reveal recent remarks about payment practice, helping you avoid a cash-only disappointment. It’s also prudent to carry a small amount of cash as a backup; even in cities where card acceptance is near-universal, a quick cash option avoids any disruption if a reader malfunctions or a vendor’s hardware battery dies in the middle of service. For the most seamless experiences, seek trucks that explicitly advertise multiple payment options, including contactless methods; such visibility is a practical indicator of a vendor’s commitment to efficiency and guest satisfaction.

An understated but meaningful way to think about the broader ecosystem is to regard the payment shift as part of a larger transformation in street commerce—one where logistics, technology, and consumer expectations converge. The shift isn’t just about a reader at a window; it’s about how a truck integrates with the rhythms of a city’s urban life. Parking networks and the routes trucks choose can influence when and where customers can interact with merchants, which in turn affects how quickly and easily payments are completed. This nested dynamic—where payment acceptance, business logistics, and consumer behavior shape each other—helps explain why card readers are now a common feature in many urban taco trucks, yet not universal. It’s a nuanced equilibrium rather than a binary transition, and it’s a sign of a healthy, adaptive street-food sector that keeps pace with a digital economy while remaining responsive to the diverse realities of city life.

For readers curious about the broader infrastructure that supports this urban shift, consider the way parking networks and truck operations intersect with payment practice. A closer look at spaces where trucks congregate shows how logistical design can enable smoother card transactions. In a practical sense, trucks that partner with stable parking networks or platform ecosystems tend to offer more consistent card access, since predictable parking supports reliable customer flow and easier tap-to-pay experiences. To explore this dimension of truck operations, see the discussion around secure parking networks at the Freight Ninja community platform: Freight Ninja Secured Truck Parking Network. This connection between physical space and payment ease helps explain why certain urban clusters feel card-friendly while others lag.

Ultimately, the practical reality in major cities is that debit and credit acceptance at taco trucks has become effectively expected in many contexts, even as pockets of cash-first practice persist. The 2025 mobile-food-service landscape reveals a market steadily tipping toward digital payments, with card acceptance becoming a default rather than a special option. Vendors who want to maximize sales recognize that offering multiple payment methods reduces friction, accelerates lines, and contributes to repeat visits. Diners, meanwhile, benefit from choice, speed, and the ability to track expenses or receive receipts without digging through cash. The interplay between consumer expectations, vendor costs, and the operational rhythms of street food suggests a future where most taco trucks in major metros routinely take debit and credit, while a minority continue to rely on cash by design or by circumstance.

External resource for further context on broader trends in mobile food service: https://www.restaurant.org/research/mobile-food-service-trends-2025

Tap-to-Taco: The Rising Role of Debit Cards in the Mobile Taco Truck Experience

Across the urban landscape, the taco truck has become more than a quick bite on the go. It is a moving intersection of culinary craft, street economy, and evolving payment technology. The question of whether taco trucks take debit cards cuts to the heart of how these fleets balance speed, reliability, and customer expectations. The reality is not uniform. Some operators embrace card readers with ease, while others still rely on cash as the accepted currency. This variability is less a failure of modernization and more a reflection of the diverse realities these mobile businesses navigate every day. A snapshot from several years ago—a Yelp review that highlighted a specific truck’s cash-only policy—reminds us that plans and preferences can diverge sharply from one stop to the next. Yet broader patterns reveal a growing openness to digital payments, driven by the practical benefits for both customers and operators. In many cities, including rapidly growing culinary hubs, card payments are increasingly treated not as a novelty but as a baseline expectation. For the seeker in a hurry or the diner who prefers digital records, the ability to pay with a debit card often mirrors the wider shift toward frictionless, data-friendly commerce.

To understand why debit cards have become more common at taco trucks, it helps to step back and look at the mechanics of the business. A food truck’s overhead is lean, but so are its margins. Cash handling imposes its own costs—manual counting, float management, risk of theft, and the need for secure on-site storage. Card readers reduce these frictions by digitizing transactions, speeding line flow, and offering a transparent trail for both the operator and the customer. In practice, this means less time spent fumbling with bills and coins and more time focused on cooking and serving. The shift toward card payments is not just about convenience; it also enables operators to upsell, track sales more accurately, and process higher-ticket orders with ease. Many vendors report that accepting cards accelerates throughput during lunch rushes and peak hours, when urban customers are in motion and every second counts. Still, the equipment and connectivity required for card processing introduce their own set of variables, especially in environments where power supply or internet reliability can be intermittent. This tension between reliability and upgrade is a recurring theme in the mobile-food ecosystem.

The decision to accept debit cards often hinges on practical trade-offs. For many operators, the initial barrier was the cost and complexity of card processing. A small but real consideration is the per-transaction fee that comes with card sales, which can feel daunting when a truck’s average order size is modest. Over time, however, the economics have shifted. Card readers have become cheaper, more durable, and easier to install, sometimes operating offline with periodic syncing. The ability to accept contactless payments adds another layer of convenience, allowing customers to tap their debit cards or phones and move on. In dense urban corridors where customers expect speed, contactless payments aren’t a luxury; they are an amplification of throughput. Still, not every truck can sustain a constant internet connection or has the right mounting for a reader, and some operators choose to run cash-only at certain locations or events where connectivity is unreliable or where cash handling is part of the operation’s culture.

From a customer perspective, the appeal of debit cards is straightforward. It’s about flexibility, speed, and safety. People often arrive with a handful of coins and bills or with a card stored in a digital wallet, and the ability to pay with their preferred method reduces the cognitive load of ordering. This is especially true for visitors who travel to food-truck hubs or spend a day wandering through a city’s street-food scene. The option to pay by debit card can influence where someone chooses to line up, how much they’re willing to order, and how generous they are with tips. The reminders that some trucks still prefer cash are not signaling stubbornness but rather honest acknowledgment of operational realities—wifi strength, power access, and the physical layout of a given site can all constrain a truck’s ability to process digital payments. In places where visibility into payment options is inconsistent, travelers are wise to check ahead—via social media posts, the truck’s official site, or local review platforms—to confirm whether debit cards, credit cards, or mobile wallets are accepted.

In growing urban markets, the adoption curve tilts toward card-based payments. In cities like Austin and Houston, for example, a notable share of mobile vendors have integrated card-readers into their setup. This integration is frequently framed as a response to customer demand—more people traveling with cards than ever before—and to the economics of speed and accuracy during busy hours. The trend is not merely about replacing cash with plastic. It’s about equipping a moving business with the tools to compete with brick-and-mrown venues that already operate on card-first principles. Trucks that successfully embrace digital payments often pair card acceptance with other digital conveniences: clear signage that indicates accepted methods, a mobile-friendly payment interface, and the ability to process contactless transactions. The result is a smoother customer journey from the moment someone first spots a queue to the moment they receive their steaming-hot plate of tacos.

The broader landscape of payment acceptance is nuanced. Some operators choose to experiment with different configurations of readers and networks, so they can adapt to outdoor environments where weather, wind, and crowd size can alter the reliability of a given device. Others lean into the immediacy of cash for small purchases or for customers who prefer not to link a card to a particular truck. In this sense, the question isn’t simply “do they take debit cards?” but rather “under what conditions do they take them, and how seamlessly can the transaction happen?” For customers, this means being prepared to accommodate a range of possibilities. Carrying a small amount of cash as a backup remains prudent in many contexts, especially when visiting a truck that parks at a busy corner, an all-day event, or a neighborhood with limited network coverage. For the diligent traveler, the best practice is to verify payment options before approaching the line. A quick glance at a vendor’s posted payment methods can save time and prevent frustration.

The ways in which taco trucks present their payment options have also evolved. In addition to signage on the truck, many operators publish payment method details on social channels or review pages. These updates are particularly common in cities where a dense network of trucks operates in a compact space. The online ecosystem around these businesses has grown to include associations that map vendors and their practices. For customers, consulting these resources can be surprisingly informative when planning a food-truck crawl or a quick lunch detour. The reality is that payment acceptance is a moving target, influenced by individual vendor choices, local regulations, and the unique challenges of mobile food service. As a result, a customer-centric approach—checking ahead, carrying a small cash reserve, and being ready to adapt to a given truck’s setup—offers the most reliable path to a smooth purchase.

For operators committed to efficiency and sustainability, card acceptance also aligns with broader portable-food practices. The digital transition can include not only payment methods but also how a truck manages receipts, inventory, and customer relationships. When operators adopt card readers and digital wallets, they often pair these tools with transparent communication about what is accepted. Reading a truck’s posted payment options becomes part of the ritual of ordering, much like choosing toppings or deciding between a soft or crunchy shell. In this light, the question of whether taco trucks take debit cards becomes a lens into a larger story about adaptability, customer-centered design, and the evolving nature of street-level food commerce. The narrative is not about forcing every truck to be a carbon copy of a retail storefront; it is about recognizing that each mobile unit tailors its payment approach to its own constraints, audience, and neighborhood rhythms. And in many cases, the result is a practical, efficient, and increasingly inclusive ordering experience that benefits both customers and operators.

As you plan a taco-truck stop, consider a few guiding practices that harmonize expectations with reality. First, if you have a preferred payment method, verify it ahead of time. A quick check on the truck’s social page or a neighborhood review can confirm whether debit cards or contactless payments are welcome at that location. Second, during busy periods, have a backup plan. A modest amount of cash can be a lifesaver when lines move fast and connectivity falters. Third, appreciate the operational freedom that comes with card acceptance. Faster payments and better record-keeping support growth for operators who might want to expand their fleets or upgrade their equipment over time. Finally, recognize that a truck’s willingness to take debit cards can reflect broader commitments to customer experience and sustainability. The digital shift often accompanies investments in cleaner setups, better signage, and clearer communication with customers about how, when, and where payments are processed. This alignment between payment methods and overall service quality helps explain why many of the city’s mobile food vendors are leaning into card acceptance as a normal part of doing business.

For readers who want a concrete example of the historical tension between cash-only and card-enabled operations, one past review stands out as a reminder of how expectations can shape experiences. A customer traveling from out of town documented a cash-only policy at a specific truck in Austin in 2017. While that particular truck’s policy may have evolved since then, the anecdote underscores a simple reality: before you head out, a little preparation goes a long way. The same story also highlights how online platforms can preserve a diverse range of experiences—some trucks remain cash-first, others embrace the latest payment technologies, and many operate somewhere in between. The evolving pattern across the country confirms a general trajectory: debit cards are becoming more common, more convenient, and more central to the mobile dining experience, even if every truck has not yet joined the trend.

To sum up, debit-card acceptance at taco trucks is not a universal rule but a growing norm. The mobile format—low overhead, dynamic locations, and direct interaction with customers—lends itself to rapid adoption of digital-payments infrastructure. Yet the realities of connectivity, power, and cash-handling needs keep some operators cash-centric. If you approach a visit with the expectation that card payments might be available but with a backup plan, you’ll likely have a smoother experience. The best practice remains straightforward: verify payment options in advance, prepare for the possibility of cash, and enjoy the ride as the street-food economy continues to blend tradition with technology. For those who want to explore best practices in the broader ecosystem of mobile-food sustainability and digital integration, some resources discuss how these systems are evolving and why they matter for communities and operators alike. In the spirit of continuous improvement, the trend toward debit and digital payments is less about replacing cash than about expanding access and efficiency across the vibrant world of the taco truck.

External reference: https://www.yelp.com/biz/tacos-manuel-austin

Swipe and Sizzle: How Taco Trucks Learned to Accept Debit Cards in a Cash-Heavy World

Taco trucks have long stitched themselves into the fabric of late-afternoon curbside culture, turning a quick bite into a ritual of flavor and tempo. Their evolution as businesses mirrors a broader shift in how people pay for everyday pleasures. In the earliest days, many of these mobile kitchens operated on a simple premise: cash only. A few quarters jangling in a pocket could buy a tortilla warmed by sun and charcoal, while a line of regulars traded stories along with their orders. The friction of carrying cash, hunting for change, and driving to the next stop created a quiet barrier between customers and a satisfying meal. It wasn’t just about money. It was about time, trust, and the tacit social contract between vendor and eater. Whenever a truck announced a cash-only policy, it often felt like a temporary refusal to embrace the modern convenience that customers expected, the same convenience that had already become standard in brick-and-m mortar venues and larger food-service chains.

The reversal of that policy—cash to cards, and eventually to taps and swipes—did not happen overnight. It unfolded gradually as both technology and consumer habits shifted in tandem. The rise of portable card readers brought a new kind of freedom to the street. They could be attached to a truck’s counter with a quick shuffle of adapters, tucked into a pouch, and powered by a modest data connection that could be restored by a hot spot or a mobile signal. The transformation was not about replacing the cart with a terminal; it was about expanding the cart’s reach. A truck that could take a debit card could attract a broader audience, including travelers who forgot to bring cash, customers who preferred to keep digital records, and office-goers who wanted a quick, contactless option during a lunch break.

In places where the urban fabric is dense with culinary choices, such as certain vibrant neighborhoods in major cities, the adoption of card payments became a natural consequence of competition and convenience. The customer base shifted toward those who value speed and predictability. A debit card payment can cut the time a line spends at the window, reduce the risk of miscounted tips or change, and provide a traceable receipt that helps both the eater and the operator manage business records. The benefits ripple outward: higher turnover, fewer cash handling risks, and the potential for loyalty programs or discounts to be tracked digitally. For drivers who usually work in lean margins, every saved minute translates into more meals served and more opportunities to refine service.

Yet this transition was never uniform. It rested on local conditions, vendor philosophy, and the operational realities of mobile commerce. Some trucks, especially those that had roots in smaller communities or in neighborhoods with strong cash cultures, still favored cash as a simple, low-friction option. The case of Tacos Manuel in Austin—a name that appears in historical reviews as a cash-only operation as recently as 2017—illustrates how even well-loved, established vendors can cling to older payment norms for a time. Customer experiences like that Yelp entry reflect a moment when the cost of changing systems weighed against the perceived benefits. The shift, when it finally comes, is not merely about inserting a card into a reader; it is about rethinking the entire payment flow—from the moment the customer places an order to the moment a digital receipt lands in their inbox.

Today, the landscape has evolved to favor choice. A growing proportion of trucks embrace card readers not as a novelty but as a standard feature. The appeal is clear: consumers anticipate and often insist on digital payments, and food vendors respond by offering a range of options, from debit to credit to contactless mobile wallets. The technology behind these options is designed to be compact and resilient. Modern readers are small, battery-powered, and able to operate even when a signal is imperfect. They connect to a network that can be restored with a tremor of the device, allowing a payment to go through even if the truck is tucked into a street with intermittent internet service. This resilience is essential for a mobile business that moves through different districts, parking lots, and events with varying levels of connectivity.

What does this mean for the everyday diner or curious traveler? It means you can walk up to a truck with a craving for something bright, zesty, and hot, and you won’t have to calculate ahead about whether you have the right kind of money. It means you can respond to a moment of impulse with the certainty that you can pay with a card, a phone, or a wearable payment method. The social texture of the interaction remains, but the financial texture becomes smoother. The vendor is no longer tethered to the arithmetic of cash; instead, the business can scale its reach and efficiency through digitized transactions that are easy to audit and easy to track for loyalty perks or repeat business. In essence, the card reader becomes a bridge between the speed of street food and the expectations of contemporary commerce.

Still, the narrative is not one of unbroken progress. Some trucks remain cautious about or restricted in their adoption of debit or credit acceptance. They cite concerns about upfront costs, processing fees, or the perceived risk of unsettled payments during peak traffic. Others worry about the reliability of networks in crowded events or at remote pop-ups where a stable connection is not guaranteed. These concerns are not trivial, but they often fade when weighed against the long-term upside: reduced cash handling, better inventory and sales data, and a more welcoming brand image for a modern palate. The decision is rarely binary. It is a calculated balance among factors such as the truck’s typical footprint, the source of its customers, and the willingness of the operator to invest in a smoother checkout process.

What can a curious visitor do to understand a specific truck’s payment options before they commit to a visit? The guidance is practical and straightforward. First, check the truck’s social media pages or its website, where vendors increasingly post their accepted methods and any changes to payment policies. Second, read recent reviews on third-party platforms; many customers who have visited the truck will mention whether debit or card payments are accepted, and whether contactless options are available. Third, look for signage on the truck itself—the equipment is often visible at the window, and a simple “debit/credit cards accepted” sign can save a lot of confusion. In communities with formal associations of mobile vendors, such as regional food truck associations, those listings frequently include payment method notes for each operator. The combined value of these sources is trust: a visitor can plan ahead to ensure a smooth, cashless or cash-friendly experience, depending on their preference.

For operators, the adoption of card payment is part of a broader philosophy of business growth and customer care. It is not merely about accepting cards; it is about delivering a frictionless experience that reinforces a sense of professionalism and reliability. A well-integrated mobile payment setup can also educate customers about the options available, potentially guiding them toward more efficient ordering methods. As a result, many trucks now pair their payment options with clear, repeated cues about hours, locations, and any special menus for the day. This alignment between product, place, and payment creates a cohesive brand moment that travelers remember when they tell friends about where to dine at a curbside stop.

The practical takeaway for readers is straightforward: pay attention to the small signals that indicate flexibility in payment. You may find a truck that happily takes debit and mobile taps while others still rely on cash only. The best advice remains to verify before you go, because the street food world does not adhere to a universal standard, and the choices are often as localized as the flavor profiles on the menu. In the end, the core truth is that the taco truck ecosystem has stitched itself into the modern payments landscape not by replacing cash, but by expanding the toolkit available to vendors and customers alike. The result is a dining experience that remains intimate and vibrant, even as the mechanics of payment shift toward more digital, efficient methods.

For operators who want to keep pace with these changes, the question of equipment is more than a technical detail. It is a strategic decision about how a truck meets the expectations of a changing customer base. This is where guidance about equipment selection becomes valuable. Consider the broader point that the right combination of devices, processes, and training can dramatically improve throughput without sacrificing service quality. On the operational side, this means selecting hardware that can handle fluctuations in network reliability, is easy to use for staff, and integrates with basic accounting practices. It also means designing a checkout flow that minimizes confusion and keeps the line moving. A well-chosen setup can become a defining feature of a truck’s brand, signaling that the business takes customer needs seriously while remaining agile enough to adapt to new payment technologies as they emerge. For those seeking a concise primer on this aspect of the craft, a helpful resource discusses choosing food-truck equipment wisely, offering guidance on balancing cost, reliability, and user experience. choose food-truck equipment wisely.

As this evolution continues, the social and economic benefits of card payments accumulate. Customers gain speed and convenience; operators gain more complete data about sales patterns, which in turn informs menu adjustments, staffing, and scheduling. The micro-economies that circulate around a popular taco truck—street-foot traffic, late-afternoon gales of appetite, weekend events—are better coordinated when every sale can be recorded and tracked. And while every city may have its own rhythm, the trend is clear: card acceptance is increasingly the norm on the taco-truck circuit, not a rare exception. The friction that once characterized street dining when cash was king has begun to fade, even in places where the culture of cash still lingers.

The landscape remains nuanced. A truck may accept debit cards but not certain digital wallets, or may offer a cash option for those who prefer it and for whom a minor fee or network hiccup would be a barrier. The best approach for a customer is to enter a line with minimal assumptions, ready to adapt and to confirm at the window. For a truck operator, the objective is to craft a payment experience that is seamless, secure, and scalable, so that a single successful transaction can become a doorway to repeat visits and sustained growth. In this sense, the card-enabled taco truck embodies a broader shift: a small business that leverages technology to remain intimate, local, and nimble while embracing the efficiencies of a modern payments ecosystem.

External reference and further reading can be found through real-world accounts that document how early cash-only policies gradually gave way to card payments. For a snapshot of the street-level reality behind these shifts, the following external resource provides an concrete example of a truck’s historical payment stance: https://www.yelp.com/biz/tacos-manuel-austin

Final thoughts

In the dynamic world of food trucks, understanding payment options is key. As demonstrated, the acceptance of debit cards varies, influenced by vendor choice and location. However, the trend leans towards accommodating digital payments as customer demand grows. Always check ahead, especially with local vendors, to enhance your taco-hunting experience. Embrace the convenience that debit cards offer and dive into tasty adventures with ease!